Download the Withholding Tax forms (PND 1 KOR, PND 1, PND 2, PND 3, PND 53, and PND 54) to accurately report and remit withholding taxes on various payments such as salaries, dividends, and professional fees.

In Thailand, companies are required to withhold tax at source on certain payments made, such as salaries paid to employees, payments made to their suppliers for certain services or certain securities income paid to shareholders. Withholding tax is a specific method of tax collection set up by the legislator to obtain a tax deposit from the recipient of the income paid by the payer. The taxpayer must fill out a monthly form declaring the amount paid to the beneficiary and thus pay the withholding tax. The form differs according to the category of income and the status of the beneficiary. The rate of withholding tax also depends on the category of income paid and the status of the recipient of the income.

As said earlier, companies operating in Thailand are required by law to apply withholding tax when paying their employees a salary, making a payment to a service provider, or paying title or rental income to a beneficiary. The amount withheld is an income tax credit that the beneficiary must pay during the year.

An example should be taken to better illustrate the withholding tax system:

Suppose a company pays a gross amount of THB 107,000 to an accounting firm for its audit services. The rate applicable for professional fees to a Thai company is 3%. The withholding tax applies before the VAT calculation. In this case, the amount of the accounting service excluding VAT is 100,000 THB. Knowing that the withholding tax is 3%, the amount charged by the company is 3,000 THB. The accounting firm will not receive 107,000 THB but only 104,000 THB after withholding tax by the client. The amount withdrawn will be credited during the accounting firm’s tax declaration.

Clients pay part of the corporation tax on behalf of the accounting firm. The paying customer is required following payment of the tax withheld at source to issue a tax certificate as proof of deduction.

Who should pay the withholding tax?

The company is subject to payment of the withholding tax in the event of:

➤ wages to its employees

➤ rent to its owner

➤ dividends to a natural person or a company

➤ interest to a natural person or a company

➤ fees or charges for services rendered by a service provider

As soon as the company makes a payment in the above cases, it must withdraw the amount according to the rate applicable to the income category and declare it to the local authorities.

What are the rates applicable?

The applicable rate varies according to the category of income paid. It is the responsibility of the company paying a service or a salary to withhold tax correctly on the amount invoiced, before VAT, and to remit this withholding at source to the Revenue Department.

Income category

Withholding tax rate

Dividends

10%

Rental income

5%

Rental fees

3%

Transport

1%

Car park

3%

Interests

1%

Royalties

3%

Phone

2%

Advertising costs

2%

Service charges and professional fees

➤ 3% if paid to a Thai company or a foreign company with a permanent branch in Thailand. ➤ 5% if paid to a foreign company that does not have a permanent branch in Thailand.

Prizes (awards)

5%

How to pay the withholding tax?

It is a tax deducted at source monthly. Indeed, the entity having withheld at source must make the declaration of the withholding tax by filing monthly four forms depending on the categories of income paid:

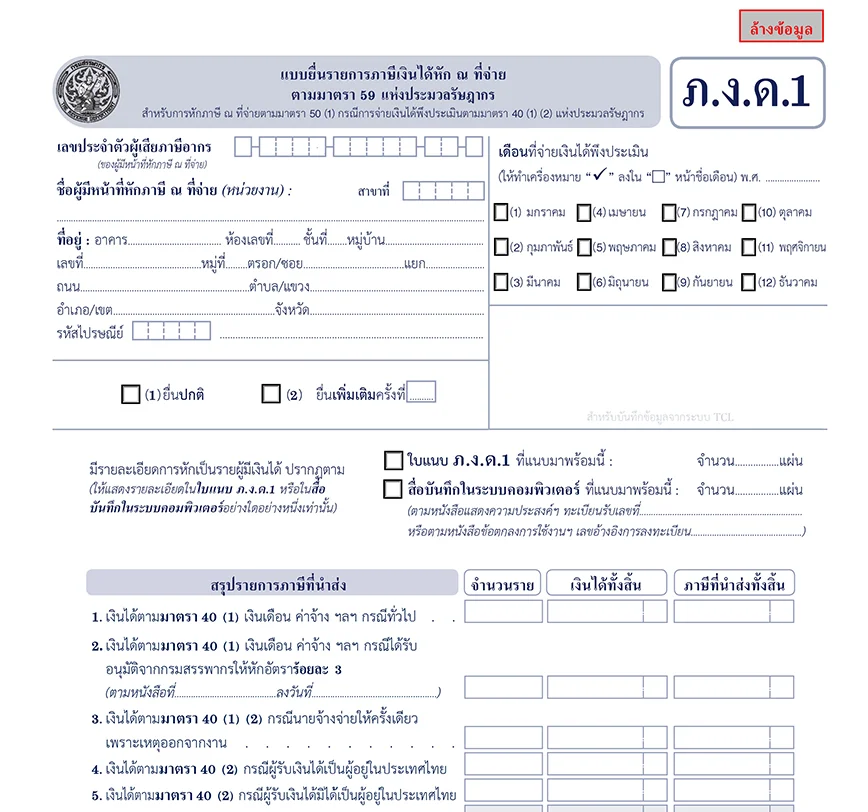

Form PND 1 for taxes withheld by the company on salaries paid to employees

Form PND 2 for taxes withheld by the company on interest and dividends paid to beneficiaries

Form PND 53 for taxes withheld by the company from vendors who are legal entities

Form PND 3 for taxes withheld by the company on sellers who are natural persons

The declaration is made to the Revenue Department at the latest within the first 7 days following the month in which the payment was made. Since January 31, 2019, companies registered for electronic tax reporting have been granted an additional eight days to submit their declaration.

For example, if the company paid the accounting firm in April, it must complete a declaration and submit the withholding tax no later than May 7 or May 15 in case of electronic reporting.

How does it work?

The mechanism of taxation via withholding tax is a complex three-person system: the corporation that pays the tax, the person receiving the income and the Revenue Department.

The corporation that pays the tax withholds part of the recipient’s income. Indeed, the company will pay a reduced payment compared to the amount provided for in the contract. Consequently, the amount withheld and not received by the beneficiary will be credited during his tax declaration. The amount withdrawn constitutes a tax credit on the final tax liability of the recipient taxpayer.

This mechanism allows the company collecting the tax to make a deposit of the tax amount on behalf of the recipient of the income.

When paying the income tax to the recipient of the income, two hypotheses are possible:

➤ Either the amount withheld is too large, the beneficiary will receive a tax refund

➤ Either the sum is insufficient, the beneficiary will have to pay an additional tax

Remarks:

It should be noted that the withholding tax levied on the beneficiary’s income does not however exempt them from making their tax declaration. Indeed, even if the tax collected corresponds to that which he must actually pay when filing his declaration, he has the obligation to submit his tax declaration annually.

What are the penalties for late payment?

In the event of a late declaration or absence of declaration, the Revenue Department sanctions the company which must withhold tax at source with a fine. For each form not submitted monthly, the company is liable to a fine of THB 200 per month with an additional penalty of 1.5% of the unpaid amount calculated monthly.

Do I have to pay when receiving rental guarantees?

In most 30-year long-term rental contracts, also called Leasehold Agreement, it is stipulated that the promoter pays rental guarantee. Once the construction of a condominium is finalized, the developer generally guarantees you a minimum return of 10% of your investment.

It is the promoter’s responsibility to withhold withholding tax on the amount of rental guarantees he pays you. It is not for the income recipient to pay.

On the other hand, you will have to complete your annual tax declaration and mention all the income that you have received regardless of the withholding tax. The tax withheld will be credited at the time of the income statement by the beneficiary.

Do I have to pay when renting an office?

If your company rents office space in Thailand, you should normally pay monthly rent to your landlord under the rental agreement. In accordance with Thai law, all rental income is subject to withholding tax at a rate of 5%. It is then up to your tenant company to pay monthly to the Revenue Department 5% of the amount of rent from which the owner benefits.

What to do when paying dividends?

In the event that your company pays dividends, you are subject to withholding tax at a rate of 10%. You must withhold at source 10% of the amount of the dividend that you pay to the shareholders of your company. In the event of payment of dividends for the benefit of one of your shareholders, your company must make its declaration the month following the payment within 7 days by submitting the form PND 2 expressly provided for income from securities regardless the quality of the beneficiary.

Remarks:

The rate applicable varies for foreign shareholders depending on bilateral tax treaties.

Can I be reimbursed for withholding tax?

It is not possible to be reimbursed. Indeed, the company which collects the tax has no right to any refund since it carries out the withdrawal on behalf of the recipient of the income. On the other hand, the beneficiary of the income who has suffered the withholding tax can claim a refund of the tax if the amount withdrawn is greater than the amount she must pay during her annual tax return.